All About Appraised Value: The Essential Guide for Property Managers

Learn how appraised value impacts property management decisions, from financing to taxes. Discover practical strategies to navigate the appraisal process and maximize your portfolio's performance.

Did you know that over 90% of property appraisals tend to be biased upward, often confirming or exceeding contract prices? This surprising statistic highlights why understanding appraised value is crucial for property managers and landlords navigating today's real estate landscape.

Appraised value forms the foundation of many critical property management decisions, from securing financing to determining fair market rent and assessing property tax obligations. As a property manager, having a clear understanding of this concept can significantly impact your portfolio's profitability and growth potential.

In this comprehensive guide, we'll explore the ins and outs of appraised value, its significance in property management, practical applications, legal considerations, and best practices. You'll gain actionable insights to navigate appraisals more effectively and leverage them to make better business decisions.

Definition and Background

Appraised value is the assessed value of a property at a specific point in time based on the opinion of a qualified appraiser. It represents the most probable price which a property should bring in a competitive and open market under conditions requisite to a fair sale, with buyer and seller acting prudently and knowledgeably.

The concept extends beyond a simple price tag. Federal regulatory agencies define market value as the price at which property would transfer under prevailing market conditions, assuming all parties are well-informed, typically motivated, and acting in their best interests. For development projects, "Value as Complete" refers to the market value once all proposed construction or rehabilitation is finished.

How appraised value is interpreted varies by context:

- In property taxation: It's the value assessed by government authorities to calculate property taxes

- In lending: It's used to determine loan-to-value ratios and mortgage eligibility

- In investment analysis: It represents the present worth of future benefits arising from property ownership

The appraisal profession has evolved significantly over time, with standardization efforts led by organizations like the Appraisal Foundation. Today's professional appraisers follow the Uniform Standards of Professional Appraisal Practice (USPAP), which provides nationally recognized standards to ensure consistency and reliability in the valuation process.

Significance in Property Management

Understanding appraised value is crucial for effective property management for several compelling reasons.

First, appraised values directly impact your operational capabilities. They form the foundation for mortgage lending decisions and risk assessment when acquiring new properties or refinancing existing ones.

The resulting loan-to-value ratios directly affect borrower credit risk profiles and the terms you can secure. Additionally, property tax assessments based on appraised values influence your ongoing operational costs, affecting everything from budgeting to rental rate determinations.

From a financial perspective, accurate valuations are essential to mortgage lending integrity. Overvaluation can create significant problems - decreasing affordability, complicating property sales or refinancing, and increasing foreclosure risk if market conditions shift.

Conversely, undervaluation prevents property owners from accessing accumulated equity and limits wealth-building opportunities that could fuel portfolio expansion.

For business growth, appraised values determine equity availability for property improvements or portfolio expansion. In a sample multifamily property appraisal, the final reconciled opinion of value was $5,000,000 with an estimated marketing and exposure time of 9-12 months - a significant figure that would substantially impact investment strategy and financing options.

For investment properties specifically, valuation directly affects capitalization rates and return on investment calculations, informing decisions about property acquisition, renovation, or disposition.

Practical Applications

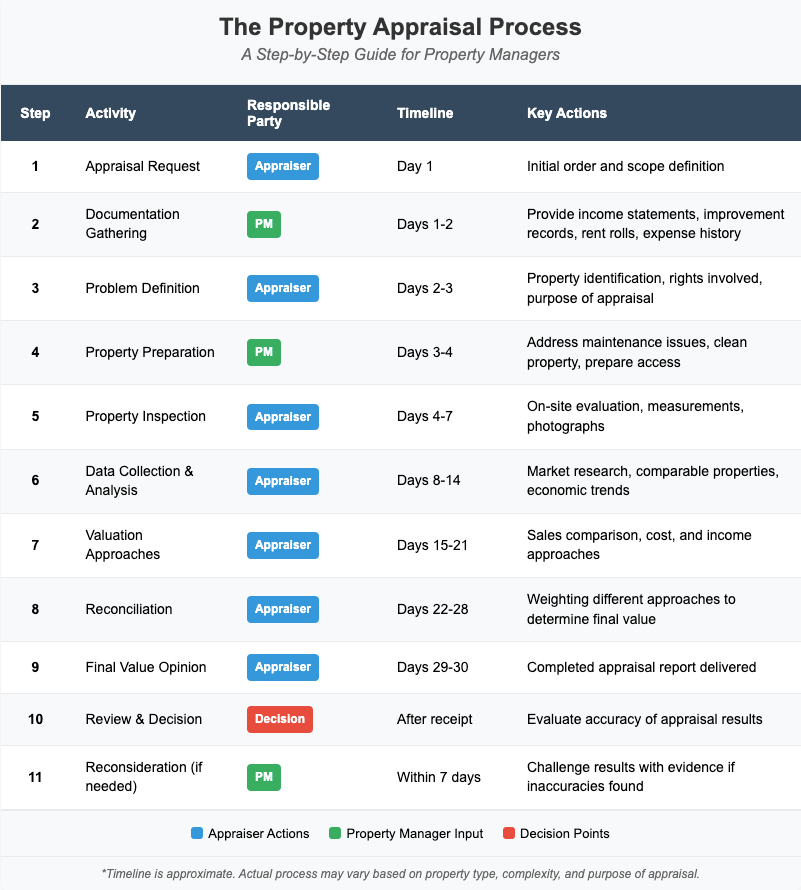

Scenario 1: Securing Property Financing

When seeking financing for a new property acquisition, financial institutions require appraisals before approving loans. As a property manager, you'll need to facilitate the appraisal process, which begins with problem definition (identifying the property and purpose of the appraisal), followed by property inspection and comprehensive data collection.

The appraiser will typically apply multiple valuation approaches (sales comparison, cost, and income) before reconciling them into a final opinion of value.

Steps:

- Prepare the property by addressing obvious maintenance issues

- Gather documentation including rent rolls, income statements, and property improvement records

- Facilitate appraiser access to all areas of the property

- Provide market context and comparable property information when appropriate

Outcome: A professionally prepared property with well-documented financials will typically yield the most accurate valuation, potentially securing better loan terms and rates.

Scenario 2: Property Tax Assessment Appeals

When government entities use appraisals to determine tax bases, the results can sometimes overvalue your property. In Texas, for example, Tax Code Section 23.01 requires appraisal districts to appraise taxable property at market value as of January 1.

Steps:

- Review the tax assessment for accuracy in square footage, property condition, and amenities

- Gather evidence of comparable properties with lower valuations

- Document property issues that negatively impact value (deferred maintenance, structural problems)

- File an appeal with the appropriate local tax authority

- Present your evidence in a clear, organized manner

Outcome: Successfully appealing an overvaluation can result in significant annual tax savings, directly improving your property's net operating income.

Scenario 3: Investment Analysis for Acquisition

When evaluating potential property acquisitions, investors use appraisals to validate purchase decisions. The approach varies based on property type and size, from single-family homes (sales comparison approach) to large apartment complexes (income approach).

Steps:

- Commission a professional appraisal focused on investment value

- Request analysis of rental market trends and vacancy rates

- Evaluate income approach calculations carefully, including cap rate assumptions

- Compare appraisal findings with your own investment criteria

- Use the appraisal to negotiate purchase price if warranted

Outcome: A thorough investment analysis based on professional appraisal helps prevent overpaying for properties and ensures acquisition decisions align with portfolio growth objectives.

Legal and Compliance Considerations

Property managers must navigate a complex web of federal, state, and local regulations surrounding property appraisals.

At the federal level, Title XI of the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA) established standards for real estate appraisals in "federally related transactions." This legislation helps ensure consistency and reliability in the appraisal process.

Additionally, the Uniform Standards of Professional Appraisal Practice (USPAP) provides nationally recognized guidelines that professional appraisers must follow. Federal banking regulations also require financial institutions to be the client in appraisals, regardless of who pays the fee.

State and local regulations add another layer of complexity. For example:

- Colorado statute § 39-1-103(5)(a) requires fee simple estate valuation for property tax purposes

- Texas Tax Code Section 23.01 requires appraisal districts to appraise taxable property at market value as of January 1

- Texas Tax Code Section 25.18 mandates property reappraisal at least once every three years

Documentation requirements are equally important for compliance. Appraisal reports must adhere to USPAP standards, including proper identification of the property, purpose, and effective date of appraisal.

Appraisers must disclose any extraordinary assumptions or hypothetical conditions affecting value conclusions, and reports must include adequate supporting documentation for all conclusions reached.

Non-compliance with these regulations can lead to significant consequences, including potential loan rejection, legal liability, and in some cases, penalties or sanctions.

Property managers should therefore maintain thorough records of all appraisal-related documents and ensure that any appraisers they hire are properly licensed and follow applicable standards.

Best Practices

1. Maintain Detailed Property Records

Keep comprehensive documentation of all property improvements, maintenance history, and financial performance. Accurate records of capital expenditures, rental income, and occupancy rates provide appraisers with the data needed for precise valuations. Update these records regularly and organize them by property, making them easily accessible when an appraisal is needed.

Implementation:

- Create digital folders for each property with subfolders for improvements, maintenance, and financials

- Document all capital improvements with before and after photos

- Maintain spreadsheets tracking historical occupancy rates and rental income

- Use property management software to generate comprehensive reports on demand

2. Develop Relationships with Qualified Appraisers

Establish connections with reputable, licensed appraisers who have experience with your property types and local markets. While you can't influence the appraisal outcome, working with knowledgeable professionals ensures a more accurate valuation process. Look for appraisers with relevant professional designations and strong local market knowledge.

Implementation:

- Research appraisers with experience in your specific property types

- Check credentials through the Appraisal Institute or state licensing boards

- Request sample reports to evaluate thoroughness and attention to detail

- Maintain a list of preferred appraisers for different property types

3. Prepare Properties Thoroughly Before Appraisals

Present your properties in optimal condition when appraisals are scheduled. Address deferred maintenance, ensure common areas are clean and well-maintained, and complete any in-progress renovations if possible. First impressions significantly impact subjective elements of the appraisal process.

Implementation:

- Create a pre-appraisal checklist covering interior and exterior preparation

- Address cosmetic issues like peeling paint or damaged fixtures

- Ensure all systems (HVAC, plumbing, electrical) are functioning properly

- Complete any minor repairs that might negatively impact value

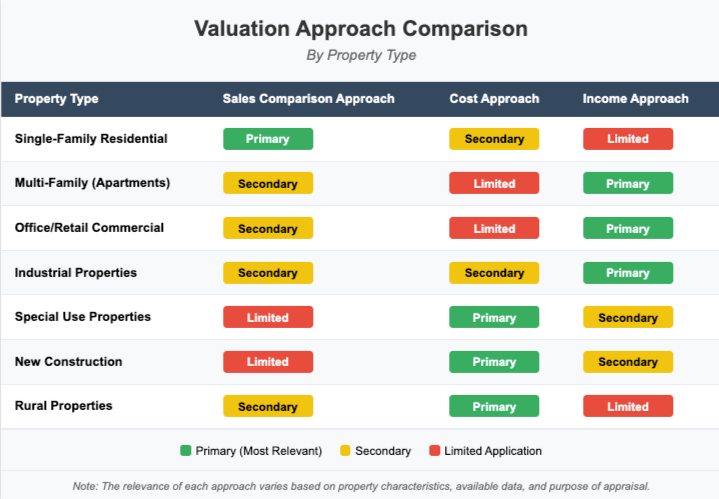

4. Understand and Apply Multiple Valuation Approaches

Familiarize yourself with the three primary approaches to property valuation: sales comparison, cost, and income. Each has strengths and limitations depending on property type.

For residential properties, the sales comparison approach is typically preferred, while income-producing properties benefit from the income approach, and special-use properties often rely on the cost approach.

Implementation:

- For single-family rentals, collect data on comparable sales in the neighborhood

- For multi-family properties, document net operating income and apply appropriate cap rates

- For newly constructed properties, maintain detailed records of construction costs

- Understand which approach is most relevant for each property in your portfolio

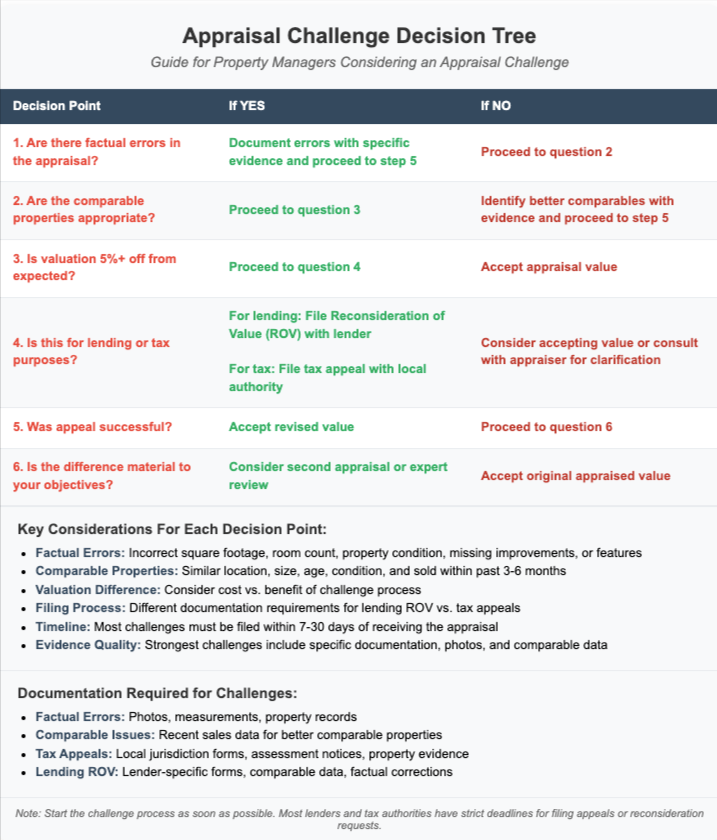

5. Establish Clear Processes for Challenging Inaccurate Valuations

Create standardized procedures for reviewing appraisals and appealing those with factual errors or inadequate comparable properties. Financial institutions offer reconsideration of value (ROV) processes when borrowers identify potential issues with appraisals. Similarly, most tax jurisdictions have formal appeal processes for property tax assessments.

Implementation:

- Review all appraisals carefully for factual accuracy and methodology

- Document specific errors or omissions with supporting evidence

- Understand lender-specific ROV processes for mortgage-related appraisals

- Know local tax appeal deadlines and procedures for property tax assessments

- Maintain records of successful appeals for future reference

Related Concepts

Highest and Best Use

This concept refers to the reasonable and probable use that will support the highest present value. It's a fundamental principle in property valuation that considers what use would yield the greatest financial return over time.

Understanding highest and best use helps property managers identify untapped potential in their properties, possibly through rezoning, redevelopment, or repurposing.

Market Value vs. Appraised Value

While often used interchangeably, these terms have distinct meanings. Market value represents what a property would likely sell for in the current market based on buyer and seller behavior. Appraised value is a professional estimate of that worth.

The relationship between these concepts is crucial when negotiating purchases, sales, or challenging tax assessments, as discrepancies can create opportunities or challenges.

Capitalization Rate (Cap Rate)

This ratio is calculated by dividing a property's net operating income by its current market value or purchase price. Cap rates are essential for income property valuation and directly relate to appraised values through the income approach. Property managers who understand cap rate trends can better anticipate how market shifts might affect their portfolio valuations.

Automated Valuation Models (AVMs)

These statistical models use algorithms to estimate property values based on comparable sales and other data. AVMs differ significantly from professional appraisals, which involve physical inspection and expert judgment.

Property managers should understand the limitations of AVMs, which cannot evaluate location details, property condition, and special features that account for approximately 30% of value determinants.

Economic Unit Analysis

This evaluation examines parcels used for mutual economic benefit, particularly relevant for multi-building apartment complexes or mixed-use developments. Understanding how properties function as economic units helps property managers make strategic decisions about acquisitions, dispositions, and property improvements that maximize overall portfolio value.

Common Questions

How does an appraiser develop the value opinion?

Appraisers develop value opinions through a systematic process that combines market research, property inspection, and analytical methods. They research market data, public records, and consult with market participants to gather information about the specific property and comparable properties.

For income properties, they estimate potential income, vacancy rates, and operating expenses, then apply appropriate capitalization rates to determine value. The process typically includes analyzing recent sales, current listings, land sales, and construction costs to provide context for the final valuation.

Can a property owner challenge an appraisal?

Yes, property owners can challenge appraisals through processes like reconsideration of value (ROV) offered by lenders. To successfully challenge an appraisal, you should identify specific factual errors in the report, point out inadequate comparable properties that don't reflect your property's characteristics, or provide evidence of potential bias in the valuation process.

Responsible lenders provide clear information about how to raise concerns regarding appraisal accuracy, and many property managers have successfully reduced overvaluations through well-documented appeals.

How do market conditions affect appraised values?

Market conditions significantly impact appraised values because appraisers must consider current market trends when determining property worth. In rising markets, comparable sales may quickly become outdated, potentially undervaluing properties, while in declining markets, recent sales might reflect higher values than current reality.

Appraisers typically apply market condition adjustments to account for these trends, but the rapidly changing nature of real estate markets means that timing can significantly affect valuation outcomes. Property managers should remain aware of local market conditions and how they might influence upcoming appraisals.

How do property improvements affect appraised value?

Not all improvements contribute equally to appraised value. Typically, improvements that address functional obsolescence, increase usable space, or modernize critical systems (HVAC, electrical, plumbing) provide the best return on investment in terms of value enhancement. Cosmetic updates like painting and landscaping improve marketability but may have minimal impact on appraised value.

Keeping detailed records of all improvements, including before and after photos, helps appraisers accurately account for value-adding enhancements to your properties.

What's the difference between appraised value and assessed value?

Appraised value is determined by a professional appraiser for various purposes including mortgage lending and property sales, while assessed value is calculated by municipal assessors specifically for property taxation.

In many jurisdictions, assessed values are a percentage of market value, often resulting in lower figures than appraised values. Understanding this distinction is important when reviewing property tax assessments and deciding whether to appeal them, as discrepancies between these values don't necessarily indicate an error.

Conclusion and Resources

Understanding appraised value is a fundamental skill for successful property management. It impacts nearly every aspect of your business, from financing acquisitions to determining rental rates and planning property improvements. By mastering the appraisal process and knowing how to prepare for, interpret, and occasionally challenge valuations, you'll make more informed decisions that enhance your portfolio's performance.

The property management landscape continues to evolve, with changing market conditions, regulatory requirements, and valuation methodologies. Staying ahead of these trends requires ongoing education and relationship-building with qualified professionals who understand your specific property types and markets.

For further learning, consider these valuable resources:

- The Appraisal Institute (www.appraisalinstitute.org) - Professional organization offering education, publications, and research on property valuation

- The Uniform Standards of Professional Appraisal Practice (www.uspap.org) - Comprehensive resource for understanding appraisal standards and ethics

- National Association of Residential Property Managers (www.narpm.org) - Industry association providing education specific to residential property management

- Building Owners and Managers Association (www.boma.org) - Resources for commercial property appraisal and management

- Local real estate investor associations - Networking opportunities with professionals familiar with local market conditions

Take action today by reviewing recent appraisals in your portfolio, identifying opportunities to improve documentation systems, and establishing relationships with qualified appraisers who understand your property types. The time invested now will pay dividends through more accurate valuations, better financing terms, and optimized property tax assessments.